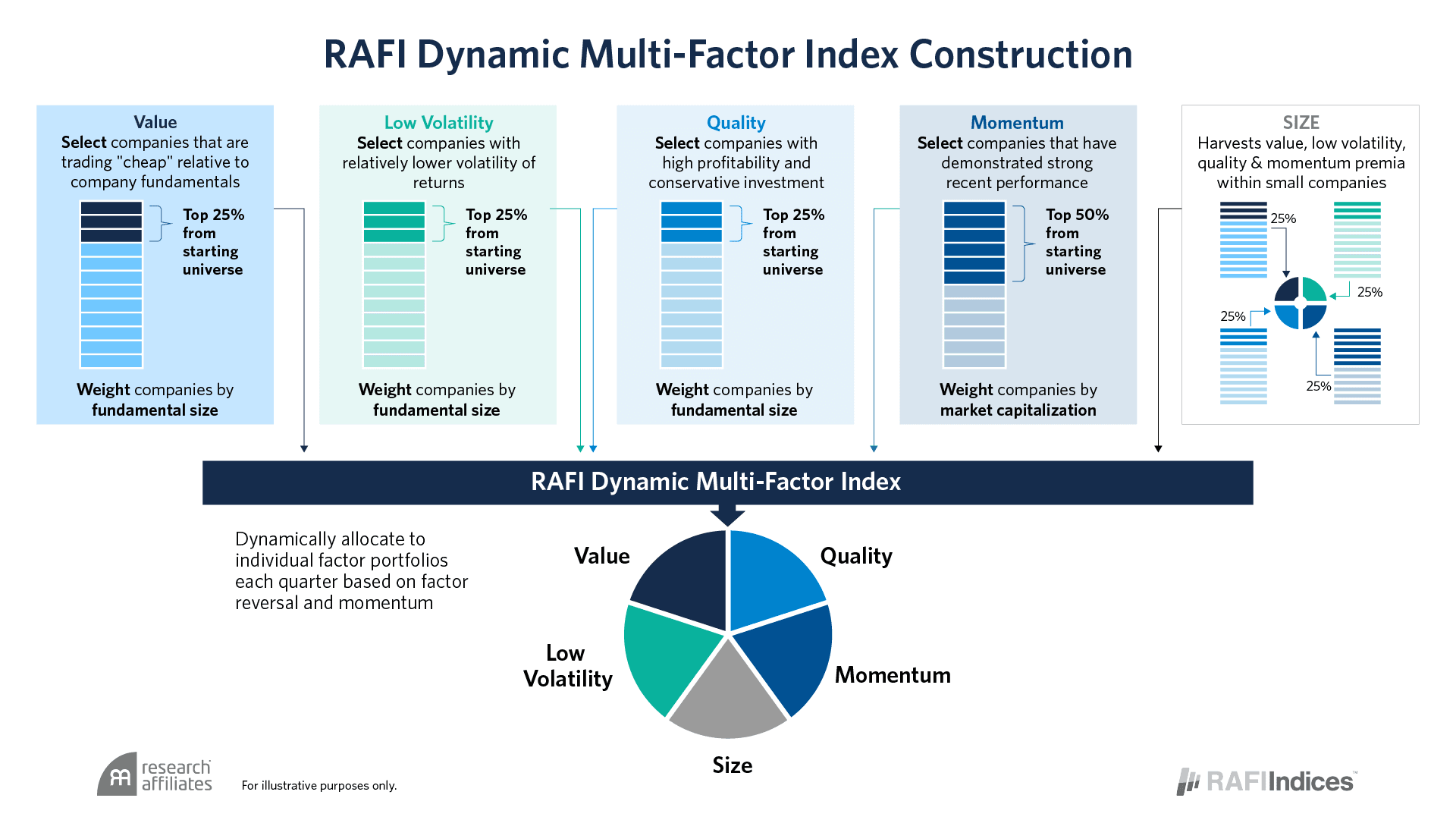

The RAFI™ Dynamic Multi-Factor Index strategy offers diversified factor exposures through time-varying allocations to value, low volatility, quality, momentum, and size.

Single-factor indices linked to robust factors (those factors supported by theoretical and empirical evidence shown to produce excess returns across multiple periods and across geographies) offer investors the potential to earn a return premium relative to market-capitalization indices. Single-factor indices, however, may have high tracking error and can be prone to long periods of underperformance. By combining multiple factor exposures, investors can achieve increased diversification and lower tracking error, resulting in a smoother path to outperformance relative to a single-factor approach.

The RAFI Dynamic Multi-Factor Index strategy provides diversified exposure to a combination of five factors (value, low volatility, quality, momentum, and size) and rebalances using a thoughtful dynamic weighting process. Our research shows that factors, like individual stocks or asset classes, go through valuation cycles and can become cheap or expensive. A multi-factor index strategy that dynamically allocates to multiple factors offers the potential for added performance.

Thoughtfully designed to deliver for investors

The RAFI Dynamic Multi-Factor Index strategy

Combines five theoretically and empirically robust single-factor strategies: value, low volatility, quality, momentum, and size.

- Value - The value premium delivers because performance chasers under-own value securities, preferring fast-growing glamour stocks.

- Low Volatility - The low-volatility premium delivers because investors’ preference for gambling leads them to over-own high-volatility securities, effectively as lottery tickets.

- Quality - The quality premium delivers because investors are attracted to the glamour of empire-building companies and underappreciate conservative capital allocators with wide economic moats.

- Momentum - The momentum premium delivers because uninformed investors are slow to react to new information about a company.

- Size – The preceding factor premiums tend to work better in small-capitalization markets because these markets tend to be less efficient and experience larger pricing errors.

Provides a diversified exposure to those factors expected to produce long-term positive excess returns. Diversifying the factors in a portfolio substantially lowers tracking error and provides shorter periods of underperformance compared to a single-factor strategy. This diversification allows for a smoother path to outperformance. Each single-factor strategy (excluding momentum) is fundamentally weighted to break the link between price and weight, thus avoiding exposure to trendy, overpriced securities

Incorporates thoughtful design and implementation that allows for straightforward performance measurement and governance. Combining the single-factor strategies to create a multi-factor index results in a transparent approach with clear performance attribution, low governance requirements, and low costs.

Offers the potential for added returns through a dynamic weighting process. Dynamically rebalancing the individual factors in the strategy, based on each factor’s long-term reversal and short-term momentum scores, results in higher allocations to factors with attractive relative valuations that are also experiencing a momentum upswing.

The RAFI™ Dynamic Multi-Factor Index strategy offers diversified factor exposures through time-varying allocations to value, low volatility, quality, momentum, and size.

Single-factor indices linked to robust factors (those factors supported by theoretical and empirical evidence shown to produce excess returns across multiple periods and across geographies) offer investors the potential to earn a return premium relative to market-capitalization indices. Single-factor indices, however, may have high tracking error and can be prone to long periods of underperformance. By combining multiple factor exposures, investors can achieve increased diversification and lower tracking error, resulting in a smoother path to outperformance relative to a single-factor approach.

The RAFI Dynamic Multi-Factor Index strategy provides diversified exposure to a combination of five factors (value, low volatility, quality, momentum, and size) and rebalances using a thoughtful dynamic weighting process. Our research shows that factors, like individual stocks or asset classes, go through valuation cycles and can become cheap or expensive. A multi-factor index strategy that dynamically allocates to multiple factors offers the potential for added performance.

Thoughtfully designed to deliver for investors

The RAFI Dynamic Multi-Factor Index strategy

Combines five theoretically and empirically robust single-factor strategies: value, low volatility, quality, momentum, and size.

- Value - The value premium delivers because performance chasers under-own value securities, preferring fast-growing glamour stocks.

- Low Volatility - The low-volatility premium delivers because investors’ preference for gambling leads them to over-own high-volatility securities, effectively as lottery tickets.

- Quality - The quality premium delivers because investors are attracted to the glamour of empire-building companies and underappreciate conservative capital allocators with wide economic moats.

- Momentum - The momentum premium delivers because uninformed investors are slow to react to new information about a company.

- Size – The preceding factor premiums tend to work better in small-capitalization markets because these markets tend to be less efficient and experience larger pricing errors.

Provides a diversified exposure to those factors expected to produce long-term positive excess returns. Diversifying the factors in a portfolio substantially lowers tracking error and provides shorter periods of underperformance compared to a single-factor strategy. This diversification allows for a smoother path to outperformance. Each single-factor strategy (excluding momentum) is fundamentally weighted to break the link between price and weight, thus avoiding exposure to trendy, overpriced securities

Incorporates thoughtful design and implementation that allows for straightforward performance measurement and governance. Combining the single-factor strategies to create a multi-factor index results in a transparent approach with clear performance attribution, low governance requirements, and low costs.

Offers the potential for added returns through a dynamic weighting process. Dynamically rebalancing the individual factors in the strategy, based on each factor’s long-term reversal and short-term momentum scores, results in higher allocations to factors with attractive relative valuations that are also experiencing a momentum upswing.

RESOURCES